BIR RMC No. 033-2026 Explained: Estate Tax Amnesty Guide for Heirs and Executors

- Yasser Aureada

- Apr 28

- 4 min read

Handling estate matters after losing a loved one is already difficult. Adding tax compliance into the situation can make it even more stressful and confusing. To address common issues and clarify procedures, the Bureau of Internal Revenue (BIR) issued Revenue Memorandum Circular (RMC) No. 033-2026, which provides guidance on the filing and payment of estate tax under the Estate Tax Amnesty program.

This article explains the circular in simple terms so you can understand what it means, how it affects you, and what steps you should take to stay compliant.

Understanding Estate Tax Amnesty

Estate Tax Amnesty is a government initiative that allows heirs to settle unpaid estate taxes with reduced penalties and simplified requirements. It was designed to encourage families to properly transfer inherited properties that may have remained unsettled for years.

However, while the amnesty provides relief, it also comes with rules that must be carefully followed. RMC No. 033-2026 focuses on clarifying these rules, especially in cases involving missing documents, undisclosed properties, and installment payments.

No Deadline for Proof of Estate Settlement—But It Is Still Required

One of the most notable clarifications in the circular is that there is no strict deadline for submitting proof of estate settlement, such as an Extra-Judicial Settlement or a court order. At first glance, this may seem like a relief for many heirs who have not yet completed their documentation.

However, this does not mean that the requirement can be ignored. The proof of settlement remains essential because it is needed for the issuance of the Electronic Certificate Authorizing Registration (eCAR). Without this document, properties cannot be legally transferred to the heirs.

In practical terms, this means that even if you have already availed of the estate tax amnesty, you should still complete your settlement documents as soon as possible to avoid delays in transferring ownership.

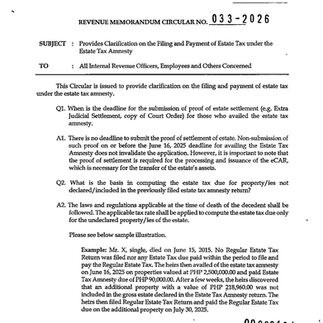

Undeclared Properties Are Subject to Regular Estate Tax

Another important point addressed in RMC No. 033-2026 is what happens when additional properties are discovered after an estate tax amnesty return has already been filed.

In such cases, the newly discovered properties are no longer covered by the amnesty. Instead, they are taxed under the laws and rates that were in effect at the time of the decedent’s death. This often results in higher taxes, especially when combined with penalties and interest.

This situation commonly happens when heirs are unaware of certain assets or when records are incomplete. Unfortunately, failing to declare all properties at the outset can lead to additional financial burdens later on.

For this reason, it is always advisable to conduct a thorough review of all assets before filing any estate tax return.

Installment Payment Is Allowed, But With Strict Conditions

The circular also confirms that installment payment of estate tax under the amnesty may be allowed. This provides some relief for families who may not be able to pay the full amount immediately.

However, this option is not without conditions. The installment arrangement must be approved by the BIR, and the full amount must be paid within two years from the statutory due date. More importantly, the first installment should have been paid on or before June 16, 2025.

Failure to follow the approved schedule has serious consequences. Missing even one installment may result in the cancellation of the estate tax amnesty privilege. When this happens, the estate will be subject to regular estate tax rules, including penalties, interest, and surcharges.

This makes it essential to carefully assess your financial capacity before choosing the installment option.

The Risk of Losing Amnesty Benefits

One of the key messages of RMC No. 033-2026 is that estate tax amnesty is not automatic or unconditional. It requires full compliance with all applicable rules.

If the requirements are not met, the benefits of the amnesty may be forfeited. The estate will then be assessed under regular tax laws, and any payments already made will only be treated as partial compliance. Additional charges may still apply, significantly increasing the total amount due.

This highlights the importance of accuracy, proper planning, and timely compliance throughout the entire process.

Why This Matters for Heirs and Property Owners

Estate tax compliance is more than just a legal obligation. It directly affects your ability to transfer, manage, or sell inherited properties. Without proper compliance, titles cannot be transferred, and assets may remain legally inaccessible.

Delays or errors can also create complications among heirs and may lead to disputes or financial strain. By understanding the clarifications provided in RMC No. 033-2026, families can avoid these issues and ensure a smoother settlement process.

How Aureada CPA Law Firm Can Help

At Aureada CPA Law Firm, we understand that estate settlement involves both legal and tax complexities. Our goal is to simplify the process and guide you every step of the way.

We assist clients in properly computing estate taxes, preparing and filing returns, completing settlement documents, and coordinating with the BIR. We also help ensure that all requirements are met so that you can secure your eCAR and successfully transfer inherited properties.

With the right professional guidance, you can avoid costly mistakes and protect your family’s assets.

Final Thoughts

BIR RMC No. 033-2026 serves as an important reminder that while estate tax amnesty offers relief, it also requires careful compliance. Understanding the rules and acting promptly can save you time, money, and unnecessary stress.

If you are currently dealing with estate matters or planning to settle an estate, it is best to seek professional advice early in the process.

Need Assistance with Estate Tax?

Aureada CPA Law Firm is ready to help you navigate estate tax amnesty and ensure full compliance with BIR regulations.

Mobile: +63 953 659 0481

Telephone: +632-3224-5601

Email: info@aureadalaw.com

Website: https://aureadalaw.com

Comments